If you’ve ever wondered whether buying a vacation home or continuing renting makes more sense, you’re not alone. The decision isn’t just about finances; it’s about lifestyle, flexibility, and long-term goals. So, is buying the right move, or does renting still make the most sense?

There’s no one-size-fits-all answer. Owning a second home offers potential financial benefits and stability but comes with costs and responsibilities. Renting provides flexibility without long-term commitments, though it doesn’t offer the other benefits.

Before making a decision, here’s what to keep in mind.

Vacation Home Market Trends

Despite higher interest rates and economic uncertainty, demand for second homes remains strong. The luxury second-home market grew by 5.2% in 2024, with the median price of high-end properties increasing by 14.2%. Meanwhile, the broader real estate market saw overall home sales decline by nearly 13%. Wealthier buyers, less reliant on loans, continue to drive second-home purchases. In early 2024, homebuyers purchased nearly half of all luxury homes with cash.1

What are the Pros and Cons of Buying a Vacation Home?

Owning a second home can be a rewarding investment but comes with responsibilities.

Potential Advantages:

- Real estate market: The value of your vacation home may increase over time, depending on market conditions.2

- Rental income opportunities: Short-term rental income may help you manage your costs.2

- Consistency and convenience: No need to book rentals or adjust to new spaces each trip.2

- Retirement: A second home could become your future residence or be sold to help support your retirement.2

Potential Challenges:

- Significant financial commitment: Beyond the purchase price, you must budget for other items, including maintenance and potential homeowners’ association (HOA) fees.2

- Property management responsibilities: Renting it out requires oversight or perhaps hiring a property manager, which could cost up to 15% of rental income.2

- Market risks: Real estate markets fluctuate, and seasonal rental demand isn’t always reliable.2

- Limited flexibility: Owning a vacation home may mean returning to the same location year after year.2

Or Is Renting the Better Choice?

Renting a vacation home offers flexibility, minimal responsibilities, and often lower costs than ownership.

Advantages of Renting:

- No long-term commitment: You can explore different destinations rather than being tied to one location.2

- Lower costs: Renting can help you manage the financial burden of ownership.2

- No maintenance hassles: The property owner handles repairs and management.2

Challenges of Renting:

- Availability concerns: High-demand vacation spots book up quickly, especially during peak seasons.2

- Lack of personalization: A rental isn’t your space, and amenities may not always meet expectations.2

- Rising rental costs: The average daily rate for vacation rentals in 2024 was $326, with luxury rentals higher.3

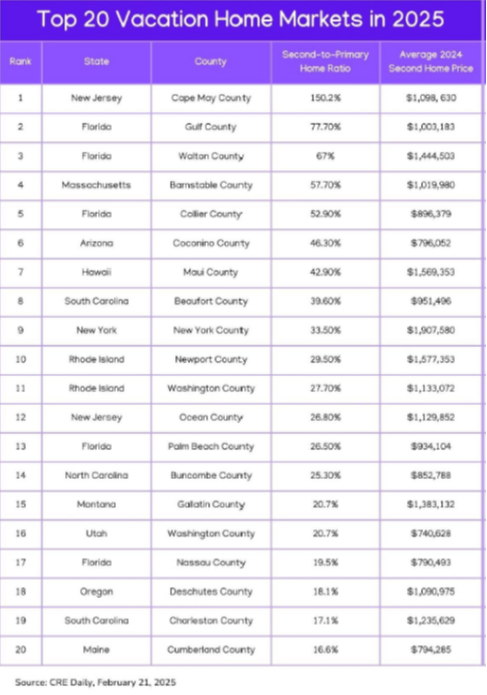

Which Vacation Spots Are the Hottest in 2025?

A CRE Daily report found these 20 counties in 2025 stand out for their increases in second home activity, the proportion of second homes to primary homes, and demand for properties priced above $700,000.1

Here’s the full ranking of the Top 20 Vacation Home Markets for 2025:

Insurance and Estate Considerations

If you purchase a second home, homeowners' insurance costs may be higher than for a primary residence. Second-home policies can cost two to three times more due to additional risks, including:

- Vacancy periods: Unoccupied homes are more vulnerable to theft or damage.

- Location-based risks: Coastal or mountainous properties may face hurricanes, floods, or wildfires.

- Rental use: Renting to others can create liability risks and require additional coverage.

If you plan to pass your vacation home down to family members, consider incorporating it into your estate strategy. Common approaches include transferring ownership or gifting the property to heirs.

Tax Considerations for a Second Home

While we are not real estate experts, we’ve compiled some information that you may find helpful. If your second home is used primarily for personal enjoyment, you may be able to deduct mortgage interest up to $750,000, depending on when the mortgage originated. However, if you rent your property for more than 14 days per year, the IRS considers it an investment property. This means:

- You may be unable to deduct mortgage interest on your personal income tax return.

- Rental fees are considered income, but certain expenses may be deductible.

- Capital gains exclusions for primary residences may not apply when selling a second home.

The Bottom Line: Weighing Your Options

Buying a second home can be a great lifestyle investment but comes with responsibilities. Renting provides more flexibility without long-term financial commitments. Whatever you decide, consider your goals, financial situation, and travel preferences.

If you’re considering a second home and want to discuss how it fits into your overall financial strategy, we might be able to provide some insights.

Sources:

1. CRE Daily, February 21, 2025

https://www.credaily.com/briefs/the-top-luxury-second-home-markets-to-watch-in-2025/

2. New Silver, January 25, 2024

https://newsilver.com/the-lender/buy-a-vacation-home-or-rent/

3. PhotoAiD, February 14, 2025

https://photoaid.com/blog/vacation-rental-statistics/